Here's a number that's hard to ignore: Americans are collectively carrying more than $1.2 trillion in credit card debt. And before you picture someone maxing out cards on luxury vacations or designer splurges, think smaller - and more familiar. We're talking car repairs, medical bills, groceries. The everyday stuff that life throws at you when your bank account isn't deep enough to absorb the hit.

The minimum payment trap

One of the sneakiest parts of credit card debt is how it grows when you're only making minimum payments. It can feel like progress - you paid something, after all - but the math is brutal. Interest compounds, the balance barely moves, and what started as a $2,000 emergency can shadow you for years. According to reporting from Vox, that debt has a way of sticking around far longer than most people expect when they first swipe the card.

Why interest rates are so high right now

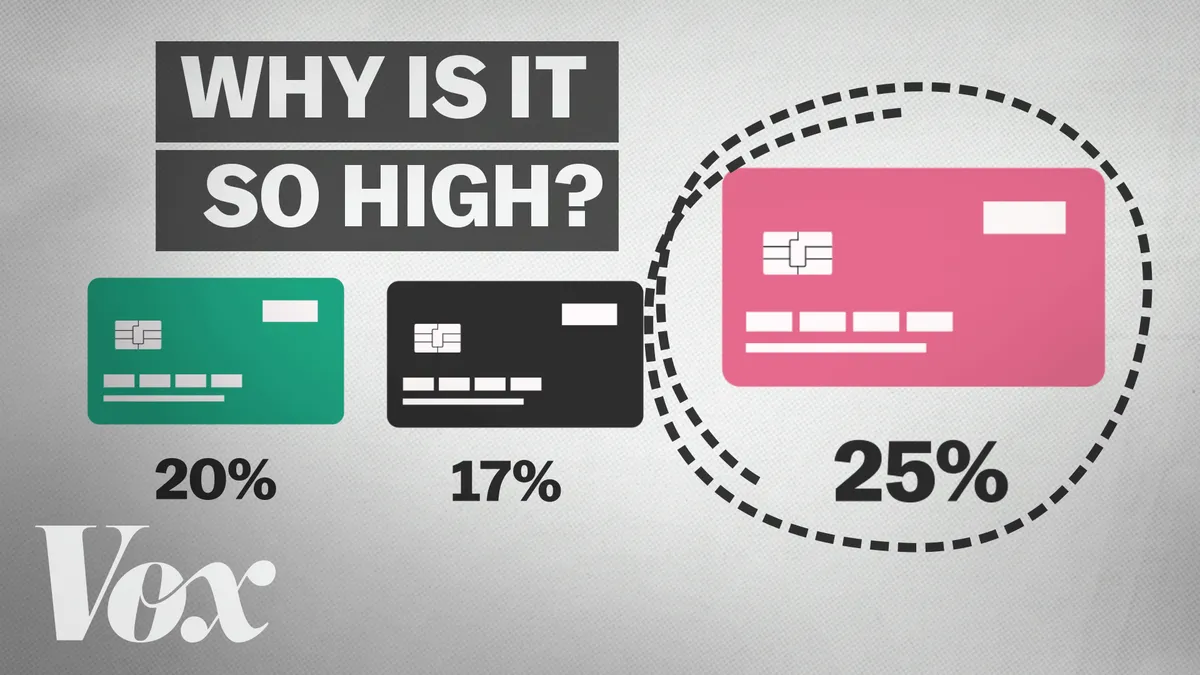

The average credit card interest rate today sits at nearly 20 percent - almost double what it was in 2010. That's not a coincidence, and it's not just greed (though that's worth discussing too). Part of the explanation is structural. When the Federal Reserve raises interest rates to fight inflation, the cost of borrowing ripples through the entire economy - including your credit card bill. Banks face higher costs themselves, and those costs get passed on to cardholders.

But the Fed's rate hikes don't fully explain a doubling of rates over a decade. The credit card industry is also enormously profitable, and in a market where most people aren't switching providers based on interest rates, there's less pressure on issuers to compete by lowering them.

Who actually feels this

The people most affected aren't reckless spenders. They're often people living close to the financial edge, where one unexpected expense - a broken transmission, an urgent care visit - becomes a multi-year debt spiral. When you don't have an emergency fund, credit cards become the emergency fund. And at 20 percent interest, that's an expensive safety net.

Understanding why these rates are so high, and how the system is designed to keep balances alive, is the first step toward making smarter decisions about how and when to use credit. It won't fix the structural problems overnight, but knowing the game you're playing changes how you play it.